The Labor Market’s Soft Rebound Continues

- Christopher Garliss

- 1 day ago

- 4 min read

ADP data showed business added 122,000 jobs in April.

JOLTS numbers showed the number of workers is equal to available jobs.

These numbers point to policy that is unlikely to change.

May’s hiring improvement looks good at first glance, but the underlying trend hasn’t budged…

Earlier this week, I laid out how I foresee the labor market taking shape. I walked through the forward‑looking indicators I track to handicap this week’s payroll report. All of them pointed to the same conclusion: May showed a rebound, but nothing to get worked up about.

That’s why I expect the U.S. Bureau of Labor Statistics (“BLS”) payroll report at the end of this week to echo that message. Even if it lands near Wall Street’s 95,000‑job forecast, that’s still well below the typical May gain of 209,000 since 2000. It would also mark one of the weakest May prints since the financial crisis in 2008-09.

Last month is usually one of the least opportune times of the year for job seekers to find gainful employment. And this week’s updates from both the BLS and payroll processor ADP confirmed the trend. Job openings and hiring improved but remain weak. That should strengthen the case for the Federal Reserve to remain on hold and helps fuel the ongoing rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

The BLS Job Openings and Labor Turnover Survey (“JOLTS”) data for April showed the number of available employment opportunities improved to 7.6 million from 6.9 million in March. That’s a drop of about 4.7 million from the March 2022 peak…

However, what’s even more important is when we compare that data to the number of unemployed people.

• By looking at the ratio, we get a sense of whether the job market is tightening or loosening.

• Tightening means employees are harder to find, driving up wages.

• Loosening means more people are seeking work, keeping a lid on pay.

• May has tended to see a rebound throughout the last decade.

In April, there were roughly 7.4 million unemployed individuals. That means there’s about 1 job available for each individual seeking work, below the five-year average of 1.3. The ratio has been around this level for the last 15 months and is hovering around pre-COVID numbers…

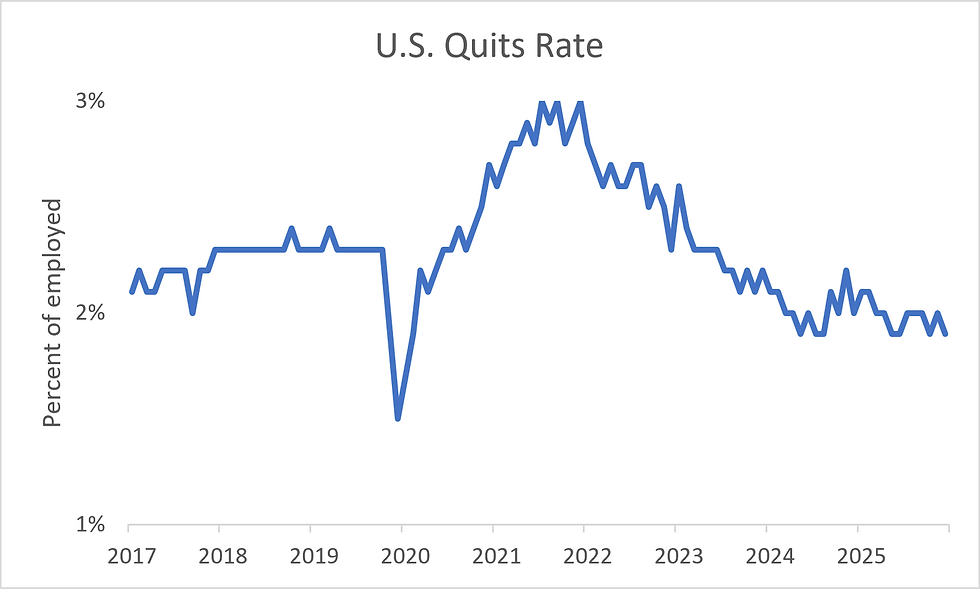

Employee turnover appears to be happening less often. The quits rate eased to 1.9%, sitting at its lowest levels outside of the pandemic…

ADP released its monthly hiring data for May. According to its estimates, companies brought on 122,000 new workers last month.

• That was up from the gain of 105,000 in April.

• It’s well below the typical May gain of 172,000 since 2011.

• It marks the 12th consecutive month of below-average hiring.

These signals matter because they shape how the Federal Reserve responds. Policymakers, including former Chair Jerome Powell, have argued that last year’s restraint on rate cuts gives them room to ride out the current inflation bump. They’re getting impatient, but they’re still willing to wait and see whether the recent jump in oil prices proves temporary. If the U.S. and Iran can strike a deal, crude could easily drift back toward pre‑conflict levels.

Bottom line: if Friday’s nonfarm payroll report lines up with the trends already in motion, Wall Street will likely grow more confident that rates stay unchanged for now, with the potential for a cut in early 2027. Lower rates next year would help reduce borrowing costs, free up cash, and support economic growth. That should continue to underpin a steady, long‑term rally in the S&P 500.

Five Stories Moving the Market:

Chipmaker Broadcom missed Wall Street expectations for second-quarter revenue while leaving a previous 2027 sales forecast unchanged; CEO Hock Tan said Broadcom now expects to ship more than 10 gigawatts' worth of AI chips in 2027 - a slight increase from previous estimates - but stuck to the company's long-range forecast of $100 billion in sales from those chips – Reuters. (Why you should care – Wall Street is increasingly concerned Broadcom could lose business at Google due to strong demand)

Israel and Lebanon have agreed to implement a ceasefire if Hezbollah also agrees to stop hostilities, according to a joint statement from both countries and the U.S.; the deal is contingent on “a complete cessation” of fire from Iran-backed Hezbollah – Bloomberg. (Why you should care – the end of hostilities between Israel and Hezbollah has been a key sticking point for Iran in ceasefire negotiations with the U.S.)

U.S. President Donald Trump has told aides privately that he would consider ending the ceasefire with Iran if Tehran kills American troops, according to U.S. officials; Trump is said to be insisting that the weekslong pause in airstrikes remains intact despite a steady stream of violent skirmishes – WSJ. (Why you should care – given Trump’s transactional nature, he likely believes that a deal is within reach)

Taiwan Semiconductor, the world's largest contract chipmaker, said it’s confident in its growth over the next few years, driven by robust demand for computing power and advanced semiconductors; CEO C.C. Wei said that its customers continue to express a positive outlook for the AI industry – Reuters. (Why you should care – Wei talked up adoption of AI models across consumer, enterprise and sovereign AI applications)

The disruption to oil and gas supplies caused by the war in the Middle East is driving a shift in Europe and Asia away from fossil fuels and internal combustion engines, and toward renewables and electric devices; the European Commission said dependence on imported fossil fuels is not only an environmental liability, it is a major strategic and economic vulnerability – Bloomberg. (Why you should care – the current Middle East crisis as well as the Russia/Ukraine conflict is driving governments to seek out more enduring solutions)

Economic Calendar:

Earnings: CIEN, COO, DOCU, LULU

RBA’s Bullock (Governor) Speaks (1:00 a.m.)

Sweden – CPI for May (2:00 a.m.)

ECB’s Lagarde (President) Speaks (4:00 a.m.)

Eurozone – Retail sales for April (5:00 a.m.)

U.S. – Challenger Job Cuts for May (7:30 a.m.)

Fed’s Barkin (Richmond, Non‑voter) Speaks (8:30 a.m.)

U.S. - Initial Jobless Claims (8:30 a.m.)

U.S. - Continuing Claims (8:30 a.m.)

BoE’s Bailey (Governor) Speaks (11:40 a.m.)

Fed’s Daly (San Francisco, Non‑voter) Speaks (1:10 p.m.)

Fed's Balance Sheet Update (4:30 p.m.)

Japan – Household spending for April (7:30 p.m.)

Japan – Overall Wage Income for April (7:30 p.m.)

Comments