A Subtle Signal in a Noisy Market

- Christopher Garliss

- 3 minutes ago

- 5 min read

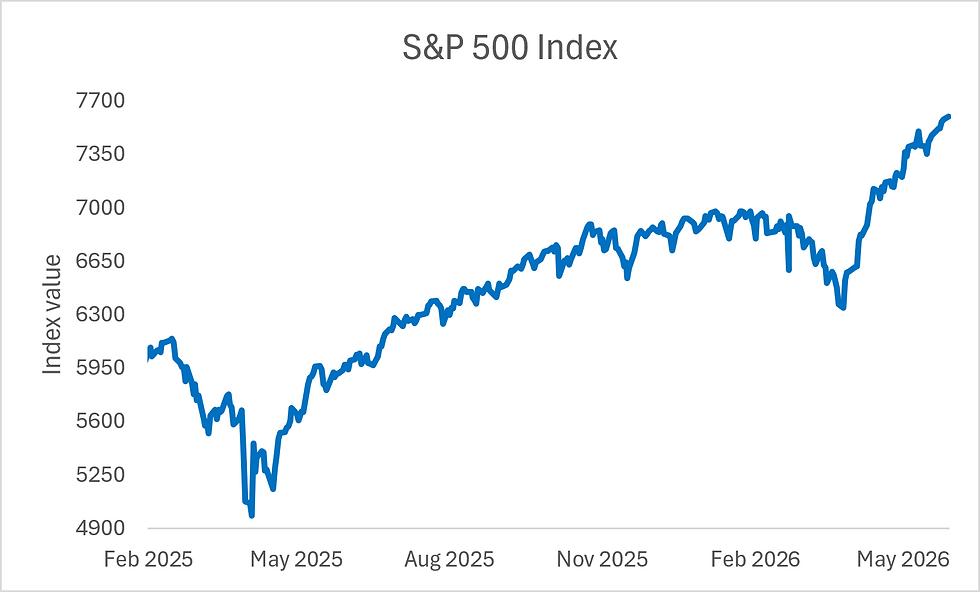

Editor’s Note: The S&P 500 just closed higher for the ninth straight session. Since 2000, we’ve seen 13 years with a streak of seven days or more. And those years typically go on to post above‑average returns.

The last time we saw a run like this was back in mid‑April. Since then, the market has climbed more than 11%. Below is the analysis I published nearly two months ago, laying out why these streaks matter — and what they tend to signal about the road ahead.

A Market Signal in the Middle of a Geopolitical Shift

The S&P 500 had a seven-day winning streak end last week.

This has happened in 13 other years since 2000.

Those years tend to produce above average index returns.

Markets tend to move long before the headlines catch up…

Over the past several weeks, one theme has kept resurfacing across our research: investors pessimism was reaching extreme levels. You could see it in the tone of institutional commentary, in the way retail sentiment gauges rolled over, and in the steady rise of cash levels across large asset managers. The backdrop wasn’t one of euphoria or complacency, it was one of caution and hesitation. And that disconnect between sentiment and data has been quietly shaping the opportunity set.

The clearest expression of that caution showed up in the positioning of systematic strategies. As we highlighted in recent notes, CTA short exposure in U.S. equities surged to extreme percentiles — 99th in the S&P 500, 97th in the Nasdaq, and 95th in the Russell 2000. These are levels that historically indicate not just elevated pessimism, but the near‑exhaustion of mechanical selling pressure. When positioning gets that stretched, the marginal seller disappears, and the market becomes increasingly sensitive to even modest improvements in news flow.

Retail investors weren’t far behind. Multiple gauges — from the CNN Fear & Greed Index to the American Association of Individual Investors sentiment survey — flashed readings consistent with deep risk aversion. Those levels were last seen in early 2025. Institutional managers were doing much the same. The National Association of Active Investment Managers Exposure Index showed a meaningful drop in equity allocations.

But that pessimism didn’t exist in a vacuum. It was unfolding at the same time the tone between the U.S. and Iran began to shift. Reports of back‑channel discussions, diplomatic feelers, and early attempts to find an off‑ramp suggested the possibility of de‑escalation. That combination of extreme investor caution and the first signs of geopolitical thawing were already laying the groundwork for a broader rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

Every so often, the market hands us a signal that’s easy to overlook in the day‑to‑day noise but meaningful when you zoom out. Last week delivered one of those moments. Between March 31 and April 9, the S&P 500 strung together seven consecutive positive closes. It was a quiet but notable show of momentum as investors recalibrated expectations around earnings, the path of monetary policy, and a potential end to the conflict in Iran.

It’s not a common pattern. This type of seven‑day winning streak has appeared in 13 other years since 2000. It gives us enough history to evaluate how the market has tended to behave after similar bursts of strength. So, I pulled the data, and tracked the S&P’s performance on both a price‑return and total‑return basis for each of those years…

What stands out is the consistency of the results. In years when this pattern has occurred, the S&P 500 has typically delivered a strong, positive follow‑through. On a price‑return basis, the index has averaged an 18.2% gain with a 92% success rate, meaning the market finished the year higher in all but one case. When you shift to a total‑return lens (dividends reinvested), the results strengthen further, with an average 20.2% gain, and again with a 92% success rate.

No single indicator is ever a guarantee, and streaks don’t drive fundamentals. But when momentum, breadth, and historical precedent line up this cleanly, it’s worth paying attention. These stretches of persistent buying often show up in the early chapters of durable market advances — and they tend to reward investors who stay anchored to the bigger picture rather than the daily tape.

As we stated at the outset, when pessimism is elevated and positioning is stretched, the market often misprices the potential for a catalyst to shift the narrative. And right now, investors aren’t prepared for a constructive outcome. Positioning is still light, sentiment is still cautious, and investors have not priced in the possibility of a cessation of hostilities in the Middle East. A credible peace agreement would remove a major risk premium, ease pressure on oil, and reset expectations around global growth and inflation.

If that happens, the combination of washed‑out sentiment, extreme CTA positioning, and improving price action becomes a powerful tailwind. Markets often move long before the headlines catch up, and this is exactly the kind of setup where a steady, durable rally in the S&P 500 can take shape.

Five Stories Moving the Market:

Japan’s cabinet approved a $19.4 billion extra budget to fund measures meant to cushion households from inflation tied to Middle East turbulence, putting fiscal policy back in the spotlight for bond investors – Bloomberg. (Why you should care – the funding for the program will come from last year’s budget measures that were cancelled)

OpenAI's ChatGPT has crossed 1 billion global monthly active app users, becoming the fastest app ever to reach the milestone, according to estimates from market intelligence firm Sensor Tower; the record comes amid growing competition between Anthropic and OpenAI for dominance in the rapidly expanding artificial intelligence market – Reuters. (Why you should care – the numbers are likely to boost demand for companies in the OpenAI supply chain like Nvidia and Oracle)

U.S. President Donald Trump signed an executive order asking artificial-intelligence companies to give the administration access to powerful models 30 days before public release; the order also asks national-security and cyber officials to work with agency heads and top tech companies to address software vulnerabilities – WSJ. (Why you should care – a previous order that had been shelved, sought a review of up to 90 days)

Canada made new and detailed proposals on trade to the U.S. based on negotiating progress in recent weeks, according to Canadian cabinet minister Dominic LeBlanc; he said recent discussions in Washington, D.C. focused on how the two sides could strengthen the relationship – Bloomberg. (Why you should care – LeBlanc said Canada is prepared for the imposition of new U.S. tariffs)

Iran is reviewing a proposed agreement with the U.S. to halt their war but has not communicated with Washington for a few days, according to Iranian media reports; Iran is pushing for a limited interim agreement as it tries to ease economic pressure while avoiding major concessions on its nuclear program – Reuters. (Why you should care – Iranian media said the government is pressing for an end to hostilities in Lebanon between Israel and Hezbollah)

Economic Calendar:

Earnings: AVGO, CRWD, M, MDT

Eurozone – HCOB Eurozone Services, Composite PMI (Final) for May (4:00 a.m.)

U.K. – S&P Global U.K. Services, Composite PMI (Final) for May (4:30 a.m.)

BoJ’s Ueda (Governor) Speaks (4:30 a.m.)

U.S. - MBA Mortgage Applications (7 a.m.)

U.S. – ADP employment change for May (8:15 a.m.)

U.S. – Fed’s Barr (Board Member, Voter) Speaks (9:00 a.m.)

U.S. – S&P Global U.S. Services, Composite PMI (Final) for May (9:45 a.m.)

U.S. – Factory Orders for April (10:00 a.m.)

U.S. – ISM Non‑Manufacturing PMI for May (10:00 a.m.)

U.S. - Energy Information Administration Crude Oil Inventory Data (10:30 a.m.)

Fed’s Beige Book (2:00 p.m.)

U.S. – Total vehicle sales for May (2:00 p.m.)

Fed’s Logan (Dallas, Voter) Speaks (4:00 p.m.)

Comments