Employment Improved in May, Yet Remains Subpar

- Christopher Garliss

- 5 minutes ago

- 4 min read

Services and manufacturing surveys show hiring rebounded in May.

Yet, the numbers are likely to remain below typical seasonality.

A below average month will keep pressure on the Fed to support growth.

The labor market woke up in May, but it’s still rubbing its eyes…

This week delivers an important update on the direction of U.S. growth. On Friday, the U.S. Bureau of Labor Statistics (“BLS”) publishes its May payroll report. Wall Street anticipates a gain of 95,000 jobs. If the number lands there, it’ll fall well short of the typical May increase of 209,000 since 2015. It would also mark another year where the labor market has remained subpar out of the gate…

Historically, May’s hiring pace runs below the annual monthly average of 227,000. Recent Fed business surveys suggested hiring rebounded last month. Yet, the increase doesn’t look like anything to get too worked up about.

If the national data echoes continued softness, it points to slow and steady growth, but a labor market that isn’t out of the woods. That backdrop reinforces the case for our central bank to stay put and possibly cut rates later this year, given a cessation of hostilities in the Middle East. That would support a continued grind higher in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

Each month, several regional Fed banks survey manufacturing and services firms to gauge business conditions. I focus on the employment and inflation components from the Dallas, Kansas City, New York, and Philadelphia districts. Together, they represent roughly one-third of U.S. GDP. Their surveys offer an early read on national trends, especially since they’re released ahead of market‑moving reports like the BLS payrolls.

Today, I’m zeroing in on employment. Let’s break down the individual components before zooming out to the broader picture.

Starting with manufacturing…

The chart above tracks the sector’s hiring trend over the past seven years.

After a pullback in January, the sector’s hiring pace appears to be stabilizing.

My gauge’s reading for May eased compared to April.

The more important services sector told a different story…

Hiring rebounded, with the gauge turning positive.

This marked the first breakout in nine months.

The overall result was still low, driven by weakness in Dallas and Philadelphia.

To get a cleaner national picture, I combined the manufacturing and services data into a single gauge. It’s weighted 80% services and 20% manufacturing, consistent with the U.S. employment mix. I also weighted each district by its GDP share…

The overall hiring picture is still soft but improving.

In May, my combined index had its first positive reading since August.

The May outcome was 0.6 compared to April’s -2.1.

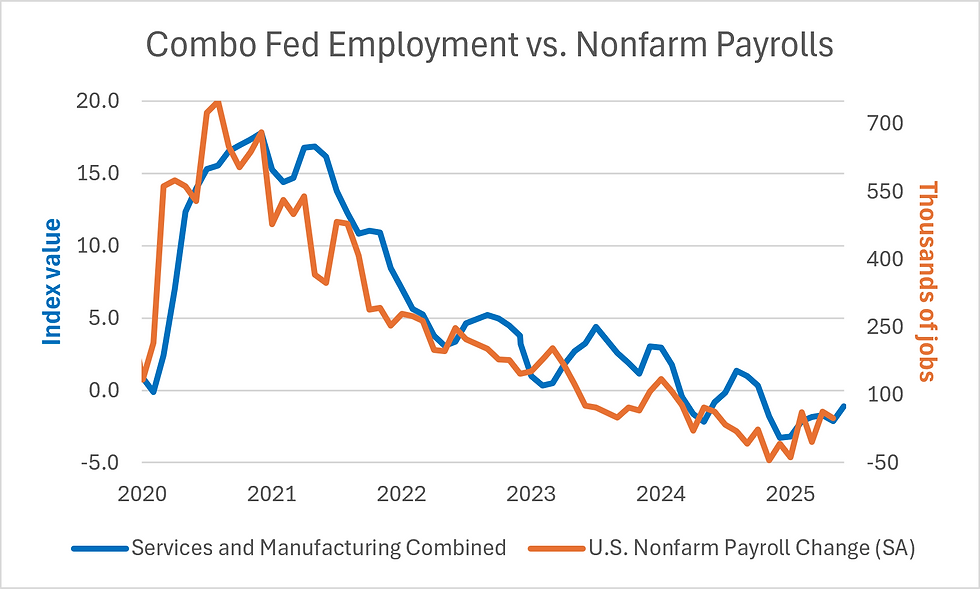

Now let’s compare the combined Fed employment gauge with nonfarm payrolls for historical context. The following chart uses a three‑month rolling average to smooth volatility and highlight the trend…

The combined Fed survey tends to lead national hiring.

The broader trend appears to be stabilizing.

Employment looks to have improved, but not by much.

At the end of the day, manufacturing and services employment has improved but remains soft. If the BLS confirms this pattern on Friday, it’ll show hiring running well below historical norms.

And if that happens, Wall Street should grow more confident in its expectation that the Fed is likely to leave interest rates unchanged for the foreseeable future. That would align with recent comments from policymakers who want to give last year’s adjustments more time to filter through the economy.

Ultimately, even lower rates by the end of 2027 would push borrowing costs down, free up cash for households and businesses, and support economic growth. That would help fuel a continued long‑term rally in the S&P 500.

Five Stories Moving the Market:

U.S. President Donald Trump asked for several amendments to the deal his envoys reached with their Iranian counterparts during a Situation Room meeting on Friday, according to senior administration officials; Trump is keen to strengthen several points that are important to him — particularly around Iran's nuclear material – AXIOS. (Why you should care – the White House expects these final negotiating points could take another few days to wrap up)

Shipowners are increasingly optimistic about a pickup in traffic through the Strait of Hormuz after more vessels left the waterway this week with the U.S. providing information to aid those making the journey – Bloomberg. (Why you should care – rising traffic through the Strait could help to drive down oil prices, easing inflation growth)

The U.S. military has not confirmed that Iran placed mines in the Strait of Hormuz despite continued searches of the critical waterway, according to U.S. officials – NBC News. (Why you should care – such a development would make it easier for safe passage across the Strait of Hormuz and allow traffic to return to normal sooner than later)

Japan’s biggest companies reduced capital spending in the first quarter even as ordinary profits at manufacturers reached a record, as emerging uncertainty from escalating turbulence in the Middle East clouded prospects for future growth – Bloomberg. (Why you should care – a drop in corporate investment could hurt the country’s growth outlook, giving the Bank of Japan reason for hesitancy on future rate hikes)

Federal Reserve Chairman Kevin Warsh has urged the central bank to pay more attention to measures like the trimmed mean inflation, turning what had been a technical debate among economists into a live question for policy – WSJ. (Why you should care – recent trimmed mean inflation data from the Dallas Fed showed price growth cooled to 2.3% in April)

Economic Calendar:

Earnings: CRDO, HPE

Fed’s Powell (Board Member, Voter) Speaks (Saturday)

Fed’s Waller (Board Member, Voter) Speaks (Sunday)

China – China Official Manufacturing, Non‑manufacturing, Composite PMI for May

China – Caixin China Manufacturing PMI for May

Japan – Au Jibun Bank Japan manufacturing PMI (Final) for May

Germany – Retail Sales for April (2:00 a.m.)

Switzerland – GDP for Q1 (3:00 a.m.)

Eurozone – HCOB Eurozone Manufacturing PMI (Final) for May (4:00 a.m.)

U.K. – S&P Global U.K. Manufacturing PMI (Final) for May (4:30 a.m.)

Fed’s Waller (Board Member, Voter) Speaks (8:30 a.m.)

U.S. – S&P Global U.S. Manufacturing PMI (Final) for May (9:45 a.m.)

U.S. – ISM Manufacturing PMI for May (10:00 a.m.)

Treasury Auctions $89 Billion in 13-Week Bills (11:30 a.m.)

Treasury Auctions $77 Billion in 26-Week Bills (11:30 a.m.)

Comments