The Skeptics Looked at AI, and Missed the Economy

- Christopher Garliss

- 5 days ago

- 5 min read

Agentic AI soaked up spare compute power capacity.

Hyperscalers plan to spend and build more to meet surging demand.

Lisa Su suggested CPU market revenue could hit $120 billion by 2030.

The turning point in the AI debate didn’t come from opinions. It came from power, steel, and CAPEX…

The debate over Artificial Intelligence has reached a turning point. For over a year, a chorus of skeptics tried to convince investors that the AI "bubble" was about to burst. They pointed to marginal productivity gains and high costs. They warned that tech giants were throwing billions into a bottomless pit.

The "bear case" for AI relied on three flawed pillars. First, critics like Michael Burry argued that tech companies were using accounting tricks. He claimed they were hiding losses by depreciating chips over five years instead of two. Second, an MIT study suggested that AI gains would be small. Finally, research from the Financial Times looked at "flat" rental rates and concluded that demand was cooling. The pessimism began to weigh on investor sentiment.

Yet, each of these arguments failed to account for physical reality. As Gavin Baker observed, a modern data center is not a real estate play. It is a power-constrained factory. A data center might have empty floor space, but it is effectively "full" if its power substation is maxed out. The NVIDIA H100 does not just compute faster; it pulls four times the power of a legacy server. This created a mirage of "excess supply" where there was actually a desperate shortage of "AI-ready" power.

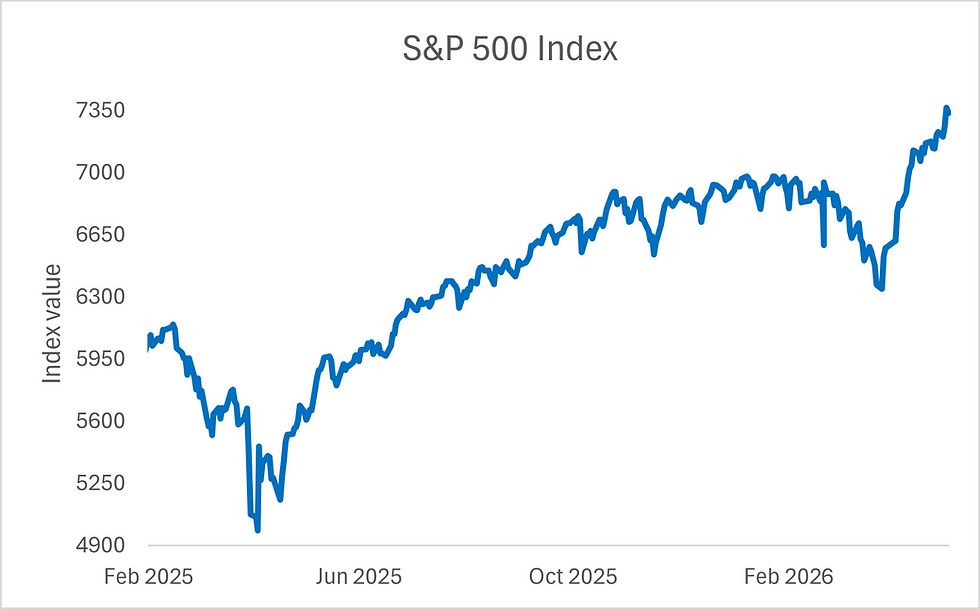

AI infrastructure is doing what few themes can: driving real CAPEX, expanding productive capacity, and pulling forward multi‑year revenue for the largest index weights. As long as transformer lead times are measured in years and hyperscaler spending is compounding, the U.S. economy has a structural tailwind. The signal is clear: the boom in data‑center infrastructure and compute power should underpin domestic economic growth and a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

The $700 Billion Signal

If AI demand were a bubble, companies would be cutting back. Instead, the 2026 earnings season shows a massive acceleration. The hyperscalers are confirmed this trend. Combined 2026 CAPEX for the top five tech giants is now projected to exceed $700 billion. Amazon alone expects to spend $200 billion, while Alphabet could double its spending.

Even AMD CEO Lisa Su has raised the stakes. She recently pointed to a server CPU total addressable market (TAM) of over $120 billion by 2030. This represents a 35% annual growth rate compared to prior guidance for 18%. These numbers prove that the world is not just buying GPUs. We are rebuilding the entire compute stack to handle a new type of workload: Agentic AI.

Agentic AI and the Inference Surge

The nature of AI has shifted. We have moved from simple chatbots to autonomous "agents." These systems do not just answer questions; they think and act for hours to finish tasks. This has turned AI from a "bursty" resource into a "persistent" one.

This shift has increased demand for the "old" chips that Burry thought would be trash. While the newest Blackwell (B200) chips handle the massive training runs, older H100 clusters are now generating massive cash through Inference. Rental rates for H100s have rebounded to from $1.70/hour late last year to$2.30+/hour as the industry faces a compute shortage. As long as a chip makes money, it stays in the rack.

The Power Bottleneck

The biggest proof of demand is the bottleneck in the power grid. We are no longer waiting for chips; we are waiting for electricity. GE Vernova recently reported a gas turbine backlog of 100 GW. Their data center orders in the first quarter of 2026 alone were greater than their entire full-year results for 2025.

Companies are now bypassing the grid entirely. Bloom Energy recently signed a massive deal with Oracle for up to 2.8 GW of on-site fuel cells. Meanwhile, industrial giants like Vertiv are sitting on a $15 billion backlog for cooling systems. Lead times for power transformers have hit a staggering 128 to 144 weeks. It’s difficult to build a "bubble" on a three-year waiting list for electrical equipment…

Bringing it All Together

The AI infrastructure cycle is just getting started. The skeptics were wrong because they viewed data centers as real estate rather than utilities. Today, an AI data center is a "Token Factory." It consumes electricity and produces high-value digital intelligence. And as each token is consumed, it generates cash for the model providers and the infrastructure owners.

The winners of this era are the "picks and shovels" companies. NVIDIA, AMD, and Amazon, among others, provide the brains. Businesses like Broadcom, Arista Networks, and Cisco provide the networking. While power companies like GE Vernova and Bloom Energy provide the lifeblood. As long as transformer lead times are measured in years, the "scarcity" of compute will drive market upside. The signal is loud and clear: Follow the flow of the electrons… because that should support a steady long-term rally in the S&P 500.

Five Stories Moving the Market:

The United Arab Emirates and buyers have recently sailed several tankers loaded with crude through the Strait of Hormuz in a bid to move oil bottled up in the Gulf by the Middle East conflict; the location trackers were shut off to avoid Iranian attacks – Reuters. (Why you should care – the passage of these ships through the Strait shows Iran does not exert complete control)

The U.S. struck military targets in Iran after the country fired on three Navy destroyers sailing in the Strait of Hormuz, an escalation that threatened to break apart a fragile ceasefire and reignite hostilities even as the two sides say they’re discussing an end to the war – Bloomberg. (Why you should care – the U.S. said it responded by knocking out the Iranian threats and retaliating against the areas from where they were launched)

Saudi Arabia and Kuwait have lifted restrictions on the U.S. military’s use of their bases and airspace imposed after the start of the American operation to reopen the Strait of Hormuz; the Trump administration is now looking to restart the operation to guide commercial ships with naval and air support that it had paused after 36 hours this week – WSJ. (Why you should care – this is a hurdle that hindered U.S. efforts to secure passage for ships through the Strait)

AI data center operator CoreWeave gave a disappointing forecast for the current quarter, sparking concerns about slowing growth; the company said revenue for the second quarter will range from $2.45 billion to $2.6 billion compared to the expectation for $2.7 billion – Bloomberg. (Why you should care – the lack of guidance upside was disappointing given the 80-% year-to-date rally)

SK Hynix is being aggressively courted by big global tech firms with offers to invest in its new production lines and fund purchases of pricey manufacturing tools as they rush to secure memory chips – Reuters. (Why you should care – the offers speak to the demand for AI-related memory products)

Economic Calendar:

Earnings: FIS, FLR, OSK, SONY, STWD, TM

Japan – Overall Wage Income for March

Japan – Au Jibun Bank Manufacturing, Services, Composite PMI (Final) for April

Germany – Exports, Imports for March (2:00 a.m.)

Germany – Industrial Production for March (2:00 a.m.)

ECB’s Lagarde (President) Speaks (3:00 a.m.)

ECB’s De Guindos (Vice President) Speaks (3:05 a.m.)

Fed’s Cook (Board Member) Speaks (5:45 a.m.)

Fed’s Bowman (Board Member) Speaks (7:30 a.m.)

BoE’s Bailey (Governor) Speaks (8:20 a.m.)

U.S. – Average Hourly Earnings for April (8:30 a.m.)

U.S. – Nonfarm, Private, Manufacturing Payrolls for April (8:30 a.m.)

U.S. – Unemployment Rate for April (8:30 a.m.)

Canada – Employment Change for April (8:30 a.m.)

U.S. – University of Michigan Consumer Sentiment for May (10:00 a.m.)

U.S. – Retail, Wholesale Inventories for March (10:00 a.m.)

ECB’s Schnabel (Board Member) Speaks (12:00 p.m.)

U.S. - Baker Hughes Rig Count (1 p.m.)

U.S. - CFTC’s Commitment of Traders Report (3:30 p.m.)

Fed Releases Balance Sheet Updates on Commercial Banks (4:15 p.m.)

Comments