The Fed's Patience Has a Shelf Life

- Christopher Garliss

- 3 minutes ago

- 5 min read

NY Fed one-year inflation expectations rose from 3.5% to 3.7%.

Three- and five-year expectations were little changed.

Lower gas prices could weigh on inflation expectations moving forward.

Inflation tells you where we’ve been but expectations tell you where we’re going. …

As noted yesterday, this week delivers an important data point for the interest‑rate outlook. Today, the U.S. Bureau of Labor Statistics releases June CPI, and Wall Street expects headline inflation to ease to 3.9% year‑over‑year. Given last month’s gasoline data, that estimate is likely close. It would mark the first pullback since January…

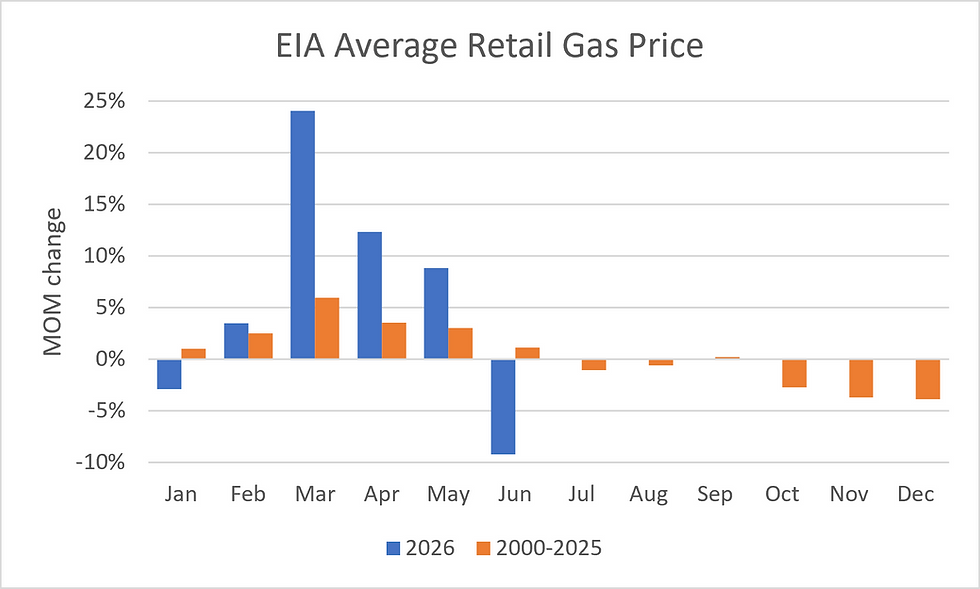

The Energy Information Administration’s latest figures show average gasoline prices fell nearly 10% in June from May. May was the high‑water mark, when WTI crude briefly touched $114 per barrel. Despite that spike, consumer inflation expectations haven’t surged. And that matters for monetary policy.

You see, the Federal Reserve worries about inflation expectations…

Policymakers know sentiment can quickly become reality.

When consumers think prices will keep rising, they change behavior now.

They buy goods ahead of time and stockpile.

Future demand gets pulled forward into the present. And if inventories plummet, the upward price pressures increase. Once that happens, our central bank must act.

The latest New York Fed survey shows expectations remain broadly anchored. Near‑term views ticked up, but longer‑term expectations held steady and remain close to historical averages. As long as they stay contained, the Fed has room to keep policy unchanged while it waits for clarity in the Middle East. That should support a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

The New York Fed recently released its Survey of Consumer Expectations for June. It summarizes responses from 1,300 households on inflation, household finances, and the labor and housing markets. The survey rotates participants to keep the sample fresh.

This survey gives policymakers a window into how people think and how they’re likely to behave. These readings matter because they show whether households expect inflation to keep climbing or drift back toward normal. Based on the latest results, near‑term expectations rose modestly…

12‑month inflation expectations increased to 3.7% from 3.5%.

The long‑run average since 2013 is just above 3.3%.

The gauge remains within its recent range.

The longer‑term picture tells the same story…

The three‑year inflation expectation increased to 3.3% in June.

The survey’s historical norm is 3%.

The latest data is also consistent with pre-pandemic levels.

Move out to five years, and the pattern holds…

Expectations stayed at 3% for the tenth straight month

That’s just above the longer‑term average of 2.8%.

This isn’t runaway inflation data.

As noted at the start, the Fed pays close attention to these numbers. Policymakers want to know how much support they can introduce for the economy without reigniting the long‑term inflation surge we saw in 2021. We’ve had a few bumps, but nothing that resembles a repeat episode, at least not according to the NY Fed’s latest read.

Given oil prices have dropped from near $114/barrel to below $80, May inflation numbers could prove to be the near-term peak. If June CPI numbers show growth is slowing, and oil prices can remain subdued, it should place downward pressure on headline inflation growth moving forward.

Fed Chair Kevin Warsh has indicated composure. Policymakers don’t want to react prematurely to developments that may prove temporary. But that patience will thin if the Middle East standoff drags into the fall.

This is why expectations data matters. If households remain anchored — and so far they have — the Fed doesn’t need to rush rate hikes. Tensions between the U.S. and Iran have intensified, but that doesn’t mean diplomacy is off the table. If inflation continues to cool, the Fed could have room to support domestic expansion by mid‑next year. That backdrop would help fuel the economy and underpin a long‑term, steady rally in the S&P 500.

Five Stories Moving the Market:

The U.S. central bank may need to raise interest rates "in the near term" if coming data show inflation continuing well above the 2% target, according to Federal Reserve Governor Christopher Waller; he said the Fed should not be "lackadaisical" if the data break in the wrong direction – Reuters. (Why you should care – Waller noted there’s still a credible case for inflation to fall back to the 2% target without changing current rates)

Federal Reserve Chair Kevin Warsh is set to deliver his first congressional testimony on monetary policy, appearing before the House Financial Services Committee today and the Senate Banking Committee tomorrow – Bloomberg. (Why you should care – with the central bank reportedly split over whether to raise rates, Warsh's remarks could offer the clearest signal yet of where policy is headed next)

The U.S. carried out its third straight night of strikes on Iran, part of a multiday campaign Trump announced alongside a new blockade on Iranian trade through the Strait of Hormuz; U.S. Central Command said the strikes aim to degrade Iran's ability to threaten shipping in the strait – WSJ. (Why you should care – the pressure campaign appears aimed at forcing Iran back to the table and dropping its claim to control Hormuz)

President Donald Trump reinstated the U.S. blockade of Iranian ships transiting the Strait of Hormuz and demanded a 20% reimbursement on all other cargo shipped through the waterway – Bloomberg. (Why you should care – Trump said the U.S. will become the Strait’s guardian while inhibiting the flow of resources to and from Iran)

The White House is seeking ways to keep power bills down for households and businesses as AI-driven data center growth strains the electricity grid; U.S. officials are planning to bring utility companies and data center developers together for a voluntary pledge – Reuters. (Why you should care – the Trump administration is trying to pull every lever it can to keep inflation growth under control)

Economic Calendar:

Earnings – BAC, C, FAST, GS, JPM, WFC

Japan – Industrial Production for May (12:30 a.m.)

China – Exports, Imports for June (3:28 a.m.)

China – New Yuan Loans for June (4 a.m.)

BoE’s Bailey (Governor) Speaks (4:45 a.m.)

U.S. – NFIB Small Business Optimism for June (6 a.m.)

U.S. – ADP Employment Change Weekly (8:15 a.m.)

U.S. – CPI for June (8:30 a.m.)

ECB’s Lagarde (President) Speaks (9 a.m.)

Treasury Auctions $95 Billion in 6-Week Bills (11:30 a.m.)

Fed’s Barr (Board Member, Voter) Speaks (12:40 p.m.)

Fed’s Goolsbee (Chicago, Non‑voter) Speaks (1 p.m.)

Treasury Auctions $69 Billion in 2-Year Notes (1 p.m.)

U.S. - American Petroleum Institute Crude Oil Inventory Data (4:30 p.m.)

Fed’s Cook (Board Member, Voter) Speaks (1:30 p.m.)

Fed’s Bowman (Board Member, Voter) Speaks (2:55 p.m.)

BoE’s Bailey (Governor) Speaks (4 p.m.)

U.S. – TIC Net Long‑Term Transactions for May (4 p.m.)

U.S. – API Weekly Crude Oil Stock (4:30 p.m.)

Japan – Reuters Tankan Index for July (7 p.m.)

Japan – Core Machinery Orders for May (7:50 p.m.)

South Korea – Exports, Imports for June (8 p.m.)

China – GDP for Q2 (10 p.m.)

China – Industrial Production, Retail Sales for June (10 p.m.)

Comments