CPI Jump, Fed Steady

- Christopher Garliss

- Apr 13

- 5 min read

Headline CPI rose to 3.3% in March.

The effective fed funds rate remains at 3.6%.

The difference means the Fed is in nor rush to raise rates.

Inflation popped in March, but the real story is how little it changed the Fed’s hand…

The stock market narrative last week was consumed by the conflict in Iran. Heading into the weekend, U.S. negotiators were scheduled to meet their counterparts in Islamabad, Pakistan, to begin hashing out the terms for peace. And while the two sides didn’t walk away with an agreement, they did emerge saying progress had been made on several fronts. That alone marked a shift from the stalemate that defined late February.

But while geopolitics stole the headlines, an important economic data point slipped under the radar. On Friday, the U.S. Bureau of Labor Statistics released its Consumer Price Index (“CPI”) data for March. The non‑seasonally adjusted annualized pace of growth jumped to 3.3%, up from February’s 2.4%…

From an inflation standpoint, that wasn’t the direction investors wanted to see. After years of grinding the measure back toward 2%, a 1% monthly surge was hardly ideal. Yet it wasn’t a regime change either.

Here’s why: even with the increase, the annualized pace of inflation still sits below the effective federal funds rate. That means the real rate of interest remains positive, implying policy is restrictive, not accommodative. In plain English, the Fed doesn’t need to raise rates. If anything, the current setup should help underpin a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

As I noted at the outset, monthly CPI growth hit 1% in March. While the month typically experiences the highest rate of increase during the year, this latest result was roughly twice as high as average…

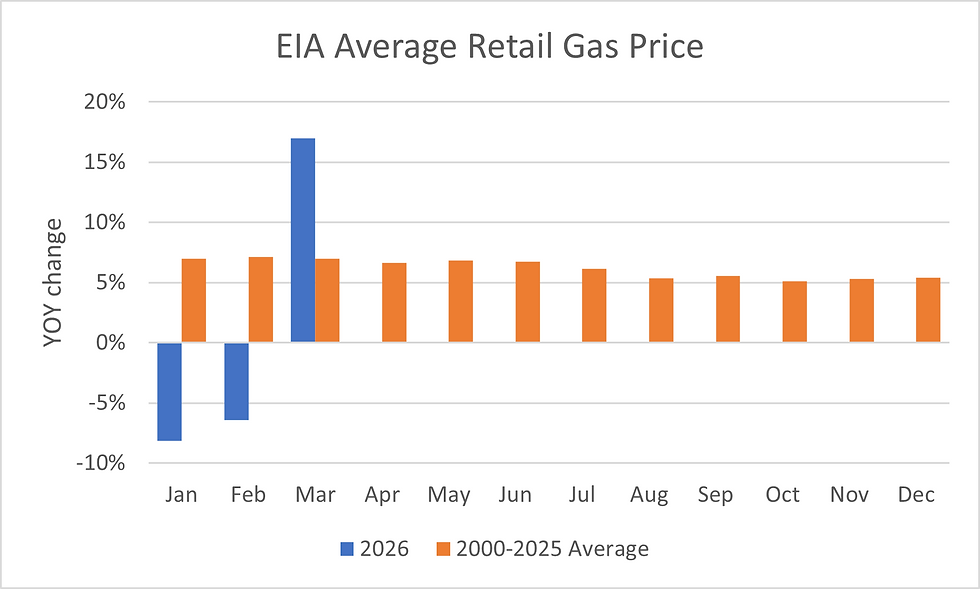

The culprit was energy. According to the Energy Information Administration, the average price of a gallon of gasoline rose 17% last month—far above the usual 7% March increase since 2000…

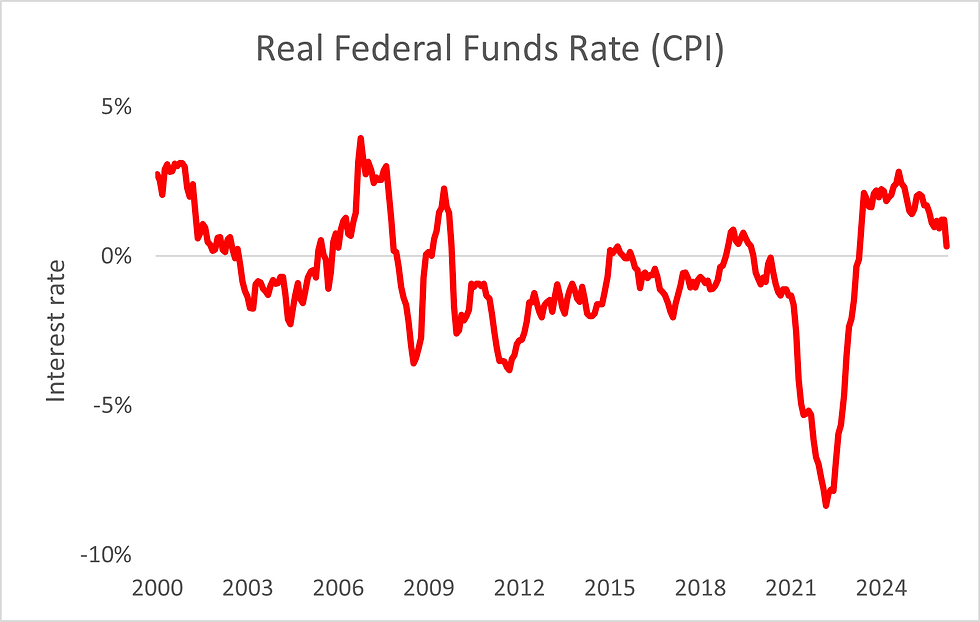

Yet the Fed has been willing to look through this. By resisting the urge to cut rates early, policymakers effectively built themselves a cushion for exactly this kind of shock. We can see this by looking at the real rate of interest. It’s a measure by which our central can monitor whether the federal funds rate is weighing on inflation growth. A positive number means policy is restrictive while a negative number means policy may be too easy.

We can calculate the number by subtracting annualized inflation growth from the effective federal funds rate. In February, when inflation was at 2.4% and the effective fed funds rate stood at 3.6%, the real rate was 1.2%. That meant our central bank had roughly 120 basis points worth of rate cut room before it hit neutral. But now, with the March inflation result having jumped, the real rate cushion has dropped to just 0.3%...

If we look at the historical data going back to 2000, we notice that the Fed may have even more room before it needs to act. According to the numbers, the real rate of interest has averaged -0.6% during that span. In other words, inflation could surge by another full percentage point before policymakers start to get nervous.

Now let’s look ahead. Prior to March, inflation growth had been averaging about 0.2% per month over the past year. So I extended that pace over the next 12 months and subtracted it from Wall Street’s expectation that the Fed will remain on hold until late 2027…

The result: real rates could briefly dip negative at the end of 2026 but then rebound quickly. By March 2027, they could climb back toward 1.2%, restoring the Fed’s cushion to cut rates again.

As I continue to note, the market isn’t irrational—it’s early. The road ahead will always be filled with uncertainty. But while pundits wait for perfect clarity, disciplined investors position for what’s next.

The U.S. and Iran are talking. That alone is progress. Both sides say movement has been made, even if the gaps won’t close overnight. If investors see more constructive dialogue in the coming weeks, concerns about Middle East–to–Asia energy flows should ease. That would weigh on global oil prices, cool inflation pressures, and strengthen the case for rate cuts next year. And that potential for easier access to money should underpin a steady rally in the S&P 500.

Five Stories Moving the Market:

President Donald Trump said the U.S. Navy would start blockading the Strait of Hormuz, raising the stakes after marathon talks over the weekend with Iran failed to reach a deal to end the war – Reuters. (Why you should care – the White House is likely trying to cut off a source of revenue for the Iranian government and apply increasing pressure to strike a deal)

President Donald Trump and his advisers are looking at resuming limited military strikes in Iran in addition to the U.S. blockade of the Strait of Hormuz as a way to break a stalemate in peace talks – WSJ. (Why you should care – the White House is discussing increased pressure on allies to take responsibility for a prolonged military escort mission through the Strait of Hormuz)

U.S. Vice President JD Vance pointed to Iran’s nuclear ambitions as the core dispute after the two sides were unable to reach an agreement during 21 hours of talks in Islamabad, Pakistan – WSJ. (Why you should care – the U.S. said it wants guarantees that Iran won’t build a nuclear weapon or seek the tools to do so)

The Federal Reserve is asking major U.S banks for details about their exposure to private credit following a surge in redemptions from the funds and a rise in troubled loans in the industry – Bloomberg. (Why you should care – regulators are likely seeking reassurance that private credit redemptions don’t pose a risk to the broader financial system)

The U.S. Court of International Trade challenged the legality of President Donald Trump's 10% tax on most imports, suggesting a large trade deficit might not be a sufficient reason to impose broad-based tariffs – Reuters. (Why you should care – the ruling could help to ease costs on imported goods and inflation growth)

Economic Calendar:

Spring Meetings of the World Bank and International Monetary Fund

Earnings: GS, FAST

China – New Yuan Loans for March (5:30 a.m.)

U.S. – Existing Home Sales for March (10 a.m.)

Treasury Auctions $89 Billion in 13-Week Bills (11:30 a.m.)

Treasury Auctions $77 Billion in 26-Week Bills (11:30 a.m.)

Comments